Stripe just made a move that I didn’t see coming, but probably should have. Their digital wallet, Link, which has been around for a while letting people store cards and bank details for faster checkout, now works with AI agents.

Yes, you read that right. AI agents can now spend money through Link. Not autonomously in the wild west sense — there are approval flows in place — but the capability is real and it’s live.

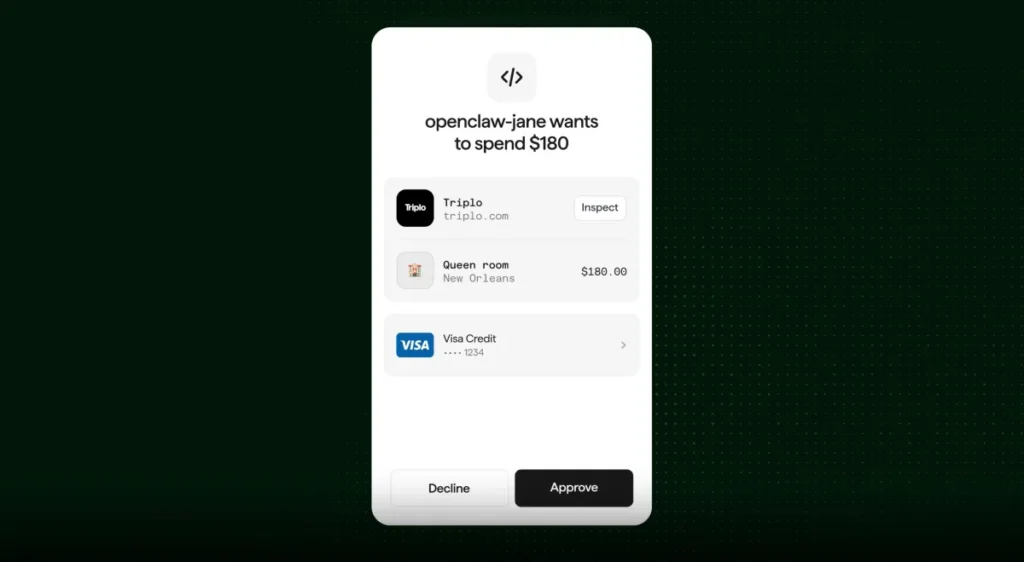

Here’s the gist: Link lets users connect their cards, bank accounts, and subscriptions in one place. The new twist is that you can authorize specific AI agents to spend on your behalf, with controls baked in. The agent requests a payment, you approve it, and the transaction goes through Link’s infrastructure.

This is higher than I expected in terms of practical adoption. We’ve been talking about AI agents booking flights, ordering groceries, and managing subscriptions for years, but the payment piece has always been the bottleneck. Stripe just removed a big chunk of that friction.

The approval flow is the key detail. It’s not a blank check — the agent can initiate, but you still have to authorize. That’s smart. It keeps the human in the loop without requiring you to manually enter card details every time an agent needs to buy something.

I’ve tested similar setups with other payment platforms, and the UX usually falls apart. Either the approval flow is too cumbersome (defeating the purpose of an agent) or too loose (risking runaway spending). Stripe’s approach with Link seems to hit a reasonable middle ground, though I haven’t gotten my hands on it yet to confirm.

What I find more interesting is the positioning. Stripe isn’t pitching this as a futuristic AI thing. They’re treating it as an extension of an existing product. That’s the right move. Link already had 100 million users as of last year, so this isn’t a new product nobody has heard of. It’s an existing wallet getting a new capability.

The practical use cases are pretty obvious once you think about it. AI agents that manage your subscriptions can now handle renewals without you digging out your credit card. Travel agents can book flights and hotels. Shopping agents can complete purchases. All through Link, all with approval flows.

But there are downsides. The approval flow still requires you to be present, which limits truly autonomous operation. If I want an agent to book a flight at 3 AM while I’m asleep, this doesn’t solve that. Stripe could add pre-approved spending limits or trusted merchant lists later, but for now, it’s still a semi-autonomous setup.

Security is another concern. Link stores payment credentials, and now those credentials are accessible to AI agents. Stripe says the approval flow prevents unauthorized spending, but I’d want to see the actual implementation before trusting it with significant amounts. The attack surface expands when you add agent access, even with guardrails.

This approach has been tried before. PayPal had similar ambitions with their developer APIs. Amazon tried with Alexa purchasing. The difference here is that Stripe is already the infrastructure layer for countless AI companies and developers. They’re not building a consumer product and hoping AI agents adopt it. They’re building a payment tool that fits into the existing AI agent workflow.

That distinction matters. Stripe’s developer ecosystem means this will likely get integrated faster than a standalone wallet ever could. Companies building AI agents can add Link support with a few API calls, rather than building their own payment infrastructure from scratch.

I’m cautiously optimistic about this. It’s not revolutionary — the core idea of agent-authorized payments has been discussed for years — but the execution matters. Stripe has the distribution, the developer tools, and the existing user base to make this work. Whether it actually gains traction depends on how well the approval flow works in practice and whether users trust it.

For now, it’s a solid step forward. Not a game-changer, but a real product improvement that addresses a genuine bottleneck in AI agent adoption. I’ll be watching to see how developers actually use it, and whether the security holds up under real-world conditions.

Comments (0)

Login Log in to comment.

Be the first to comment!